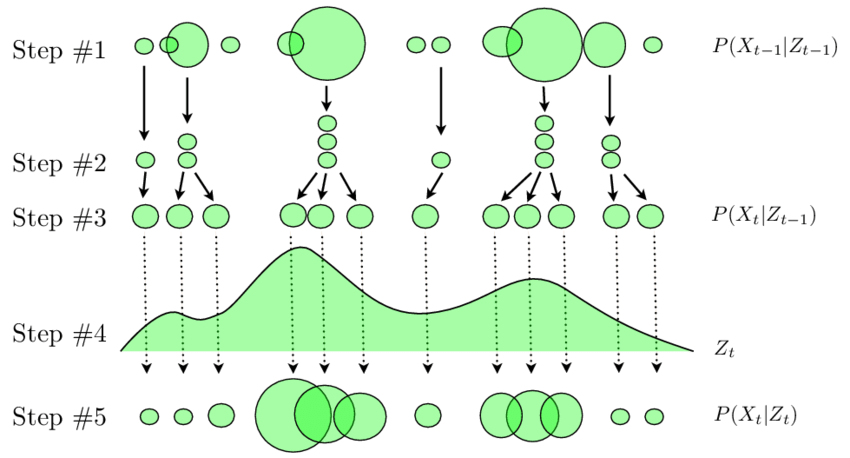

Particle Filters is a simulation technique for tracking moving target distributions. It is used for reducing the computational burden of a dynamic Bayesian analysis. The technique uses a Markov chain Monte Carlo method for sampling in order to obtain an evolving distribution, i.e., to adapt estimates of posterior distributions as new data arrive.