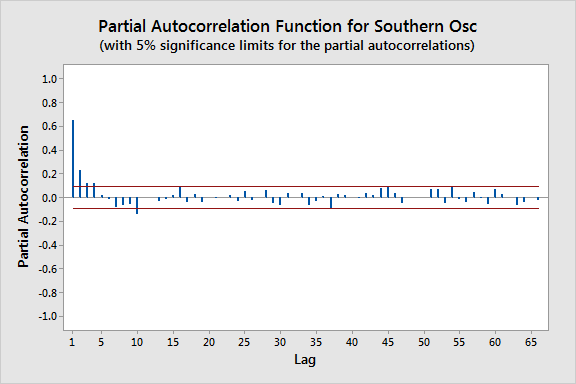

Partial Autocorrelation is a measure of the correlation between the observations a particular number of time units apart in a time series, after controlling for the effects of observations at intermediate time points. Partial Autocorrelation Post navigation Parsimony PrinciplePartial Correlation Leave a ReplyYour email address will not be published. Required fields are marked *Comment * Name Email Website